An earlier version of this article was posted in the Tax Justice Blog.

Last week, the House Ways and Means Committee held a hearing on the Tax Cuts and Jobs Act (TCJA). Proponents of the law used the occasion to tout its alleged economic benefits and argued that its temporary provisions should be made permanent. The title of the hearing was “Growing Our Economy and Creating Jobs,” but there is little evidence that the law does either of these things.

Even before Congress passed TCJA, many corporations paid 21 percent or less of their profits in taxes and many paid nothing at all.

Proponents of TCJA claimed that lowering the corporate tax rate to 21 percent would allow American companies to invest more in the United States, hire more workers and pay them better.

- Some of the biggest companies that have announced bonuses or raises for employees paid low effective rates in the five years before TCJA was enacted, including Bank of America (5.9 percent), AT&T (11.6 percent), Verizon (21.3 percent), Wells Fargo (21.4 percent) and others. If anything was holding these companies back from paying their employees better, it was not their federal tax bill.

- Plenty of American corporations managed to pay nothing in taxes before TCJA was enacted. For example, Amazon paid nothing in federal income taxes last year and paid an effective rate of just 5.3 percent over the past five years. Duke Energy paid nothing last year and paid nothing over the past five years. Prudential paid nothing last year and paid an effective rate of just 2.1 percent over the past five years.

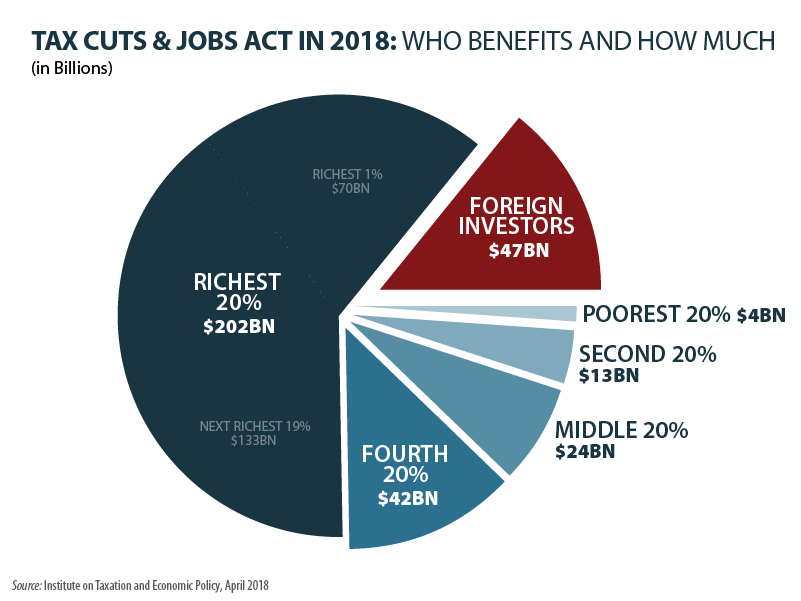

The Congressional Budget Office (CBO) has concluded that TCJA will boost incomes — but mainly for foreign investors.

The CBO concluded that the new tax law will grow the economy, but over the coming decade foreign investors will receive 43 percent of that growth and will receive 71 percent of that growth in 2028 alone.

- In part, this is because the corporate tax cuts making up a big part of TCJA benefit foreign investors, who own more than a third of the stocks in American corporations. ITEP estimates that foreign investors will receive $47 billion in benefits (because of the corporate tax cuts) from TCJA this year, which exceeds the benefits for the bottom three-fifths of Americans put together.

- Another reason foreign investors benefit is that the tax law is deficit financed (adding $1.9 trillion to the national debt) and many of the bondholders are foreigners.

- In fact, some experts believe that even the sliver of income growth left for Americans will disappear by the end of the decade.

{kind=link}

There is not much evidence that TCJA has prompted corporations to invest more in the United States.

Americans for Tax Fairness has found that the bulk of the new investments announced since TCJA became law come from just three companies. In each case the activity being touted is not truly “new” and there is no indication that is it related to the tax law.

- President Trump praised Apple for announcing plans to “invest a total of $350 billion in America,” but it turns out that Apple merely said that its “contribution to the U.S. economy will be more than $350 billion over the next five years.” The company’s actual new investments are likely to be a tiny fraction of that amount.

- Meanwhile, Comcast and ExxonMobil both have announced plans to invest $50 billion over the next five years, but this is not a meaningful increase for these companies compared to prior years. Most other announced investments by companies are in single digit billions or less.

Making the temporary provisions in the tax law permanent will not solve the new law’s fundamental tax fairness problems.

As explained in a recent op-ed by ITEP staff, some lawmakers talk as through the temporary provisions in TCJA are “middle-class tax cuts,” but this is not true. ITEP’s recent report on TCJA finds that:

- In 2018, the richest fifth of households receive 71 percent of the benefits of TCJA.

- Should Congress enact a bill to extend all the TCJA provisions that expire after 2025, the richest fifth of households would receive 65 percent of the benefits of that legislation in 2026.

- In that scenario, in 2026 the richest fifth of households would receive 71 percent of the combined effects of TCJA (the law’s permanent provisions that will still be in effect) and legislation to extend TCJA’s temporary provisions.

Steve Wamhoff is the Director of Federal Tax Policy at The Institute on Taxation and Economic Policy