It’s no secret that the U.S. public debt is out of control. It recently surpassed the size of the U.S. economy for the first time since World War II, and is slated to get even worse in the coming years. A recent Congressional Budget Office (CBO) report projects that public debt will reach a record 120 percent of Gross Domestic Product (GDP) by 2036, largely driven by successive rounds of federal tax cuts implemented over the past three decades. A broader fiscal course correction – one that raises new revenues and improves efficiency in government spending without harming the nation’s most vulnerable citizens – is desperately needed.

While lawmakers on both sides of the aisle have been sounding the alarm for decades, they have largely ignored a major contributing cause of our nation’s skyrocketing debt: declining corporate tax revenues. Congress has allowed corporate taxes as a share of total revenues to drop from over 30 percent during the 1950s to just 7 percent as of 2022. This decline is the result of successive rounds of lavish tax handouts to large corporations, including, most recently, around $1 trillion in tax breaks that were expanded and made permanent by lawmakers in 2025. Congress did so at the expense of the American public and their constituents: polling shows that more than four out of five midterm voters, including 67 percent of Trump voters, support raising taxes on large corporations.

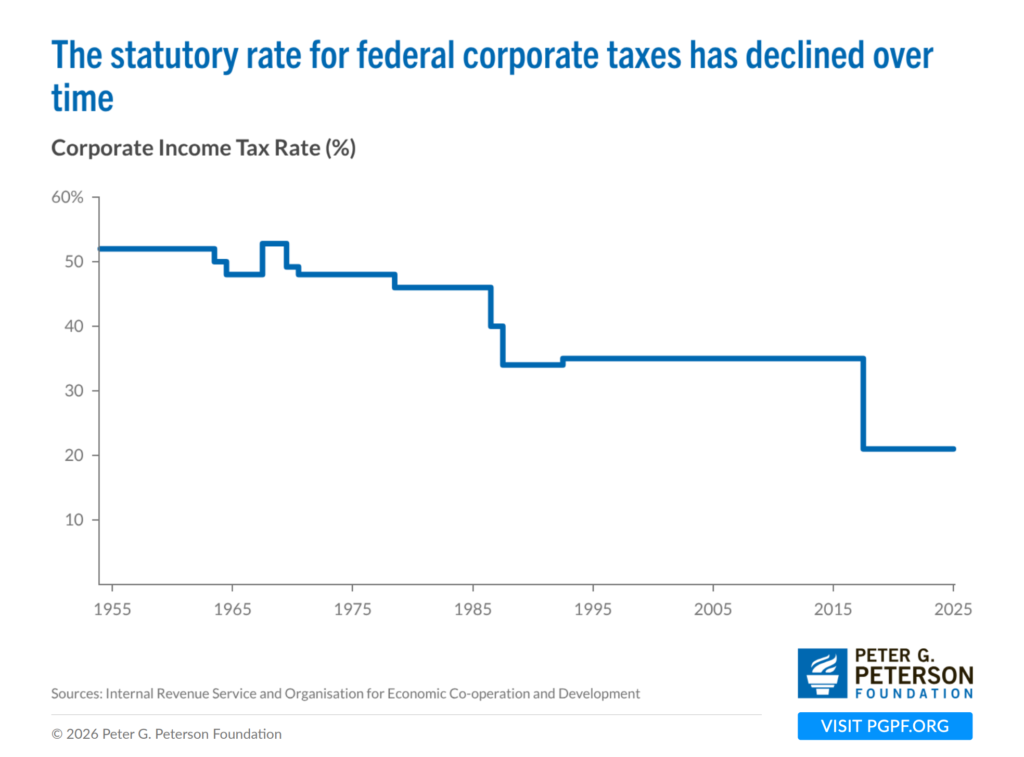

This story should not be surprising. The statutory corporate income tax rate has been cut by more than half since its peak in the 1960s to just 21 percent. Effective corporate tax rates, however, are substantially lower than the already historically low statutory rate. Analysis by the Government Accountability Office has shown that the average corporate effective tax rate plummeted to just 9 percent after the 2017 tax reform went into effect. Post-2025, marginal effective rates are expected to decline even more precipitously.

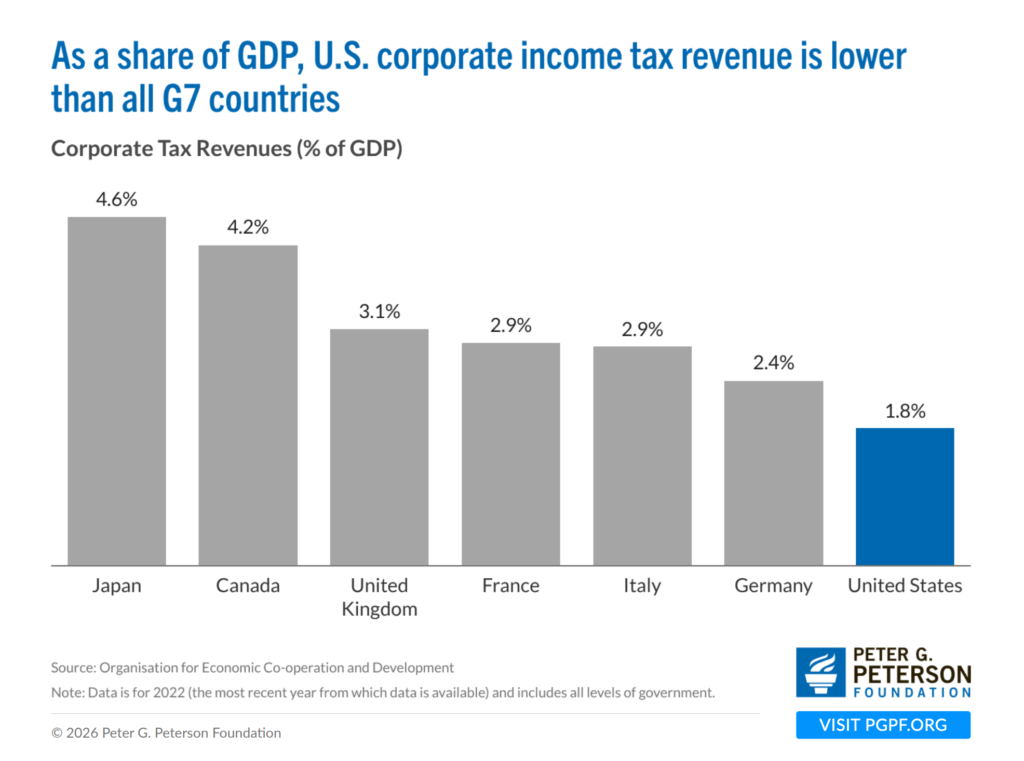

The U.S. also collects less corporate tax than other developed countries as a percentage of overall tax revenues. OECD countries collect an average of 12 percent of revenues in the form of corporate income taxes, while the U.S. collects just 7 percent of revenues from corporate income taxes.

This trend will only worsen in the coming years. While the 2025 tax reform didn’t change the statutory corporate income tax rate, it included costly international business provisions on top of dramatic expansions of corporate tax breaks like bonus depreciation and deductions for interest expenses, which will lower the effective tax rates multinational corporations pay. Congress’ longstanding failure to adequately tax the foreign profits of the nation’s largest companies doesn’t just cost the U.S. revenues: it also incentivizes the continued movement of investment and income abroad. This means fewer jobs for Americans, fewer dollars in our economy, and an uneven playing field that puts American entrepreneurs and small businesses at a disadvantage.

Commonsense reforms popular among voters of both parties could help reverse the trend of declining U.S. corporate revenues. First, Congress should equalize the tax rates that corporations pay on income earned abroad and at home, repealing the large tax discount for foreign income that companies have used to shrink their tax bills through the elaborate offshore structures. Second, Congress should get rid of wasteful tax breaks like the foreign-derived deduction-eligible income (FDDEI, formerly FDII) deduction, which rewards firms for profitable export activity they likely would have engaged in anyway.

But big corporations aren’t just shifting profits to tax havens: in many cases, they’re opting not to be taxed as corporations at all. A growing number of businesses are not taxed separately as corporate entities, but merely “pass through” their obligations to their owners. Once the domain of small businesses, these entities are increasingly large and complex, including many private equity and hedge funds, and are the vehicles by which many wealthy Americans hold their wealth in offshore tax havens. Pass-throughs earn more than half of all U.S. business income. The size and complexity of many of these businesses make them essentially un-auditable; the IRS examination rate for complex partnerships has collapsed to less than 0.1 percent in 2023.

To address these imbalances, Congress should pursue broad reforms to tax the largest pass-through businesses as corporations and make sure that the IRS has the resources necessary to effectively audit large, complex businesses, including both multinational corporations and pass-throughs. The IRS must also be well-resourced to pursue offshore tax evasion by wealthy American individuals, which runs into the billions of dollars in fines alone, even before considering back taxes.

There is no one magic bullet to address our nation’s runaway debt. Congress will need to make hard choices to both raise new revenue and improve the efficiency of federal spending. The problem will prove impossible to address, however, so long as the nation’s largest and most successful businesses continue to avoid paying meaningful levels of tax. Plenty of policymakers pay lip service to “fiscal responsibility” when it is politically convenient – if they want to prove that they are serious about tackling our fiscal crisis, then corporate tax reform should be at the top of the agenda.